Key takeaways

Fundraising timelines extended 62% since 2022. Median close climbed from 11.2 to 18.1 months.

Digital presence now pre-screens managers. Allocators research online before accepting any meetings.

Brand coherence signals operational capability. Inconsistent messaging raises concerns about organizational gaps.

Integrated communication accelerates fund closes. Coordinated strategies outperform ad hoc approaches significantly.

Start communication 12-18 months early. Lead time builds credibility before fundraising launches.

Why fundraising timelines have extended

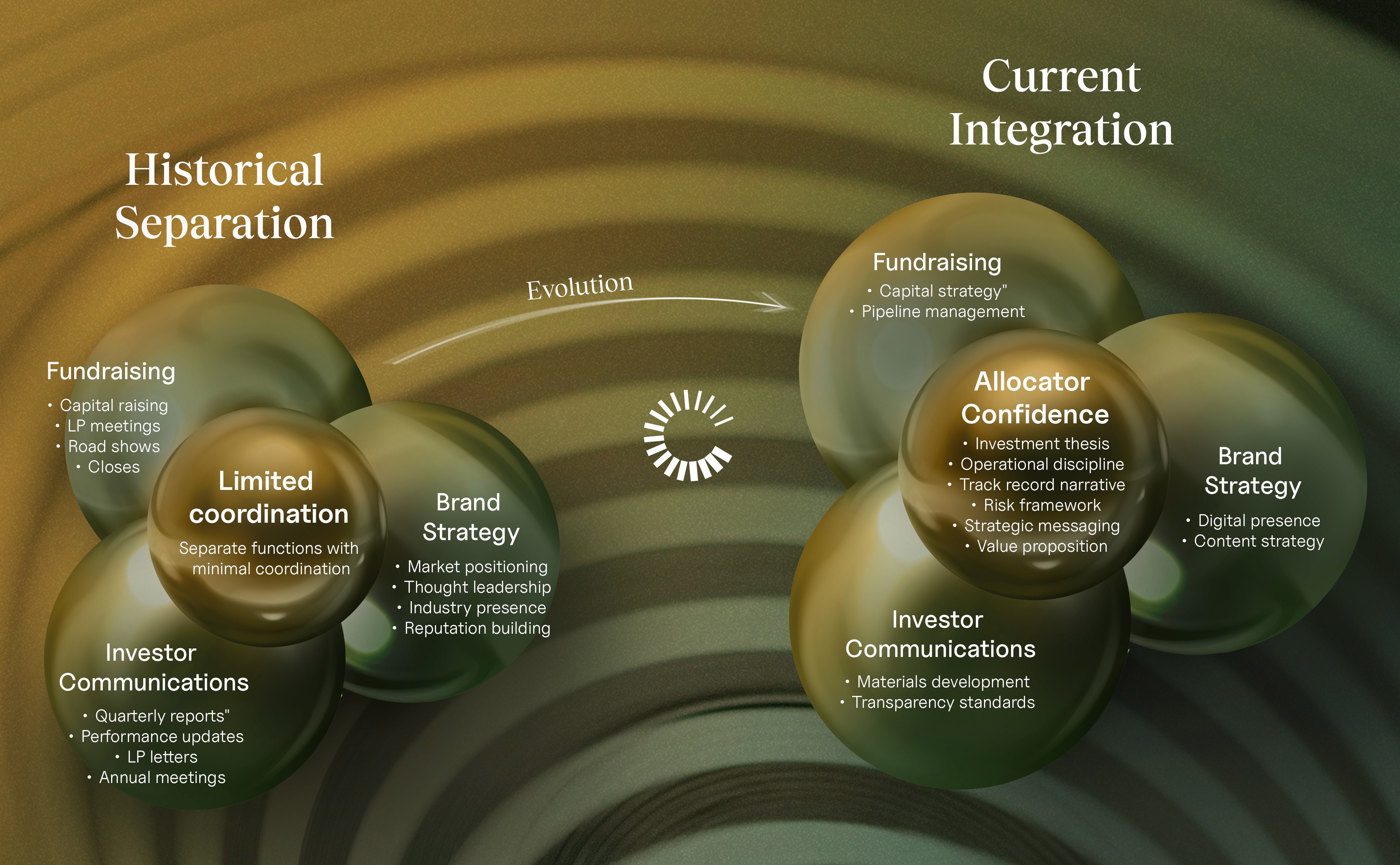

Fundraising outcomes increasingly depend on communication quality alongside performance. Allocators assess a manager’s brand, narrative, and materials early, making marketing strategy a decisive factor in capital formation.

The median time to close across US Private Equity (PE) funds climbed to 18.1 months in H1 2024, up significantly from 14.7 months in 2023 and 11.2 months in 2022. The widening gap between deal closes and protracted campaigns is about perception, not just performance.

5 forces that made communication a fundraising variable

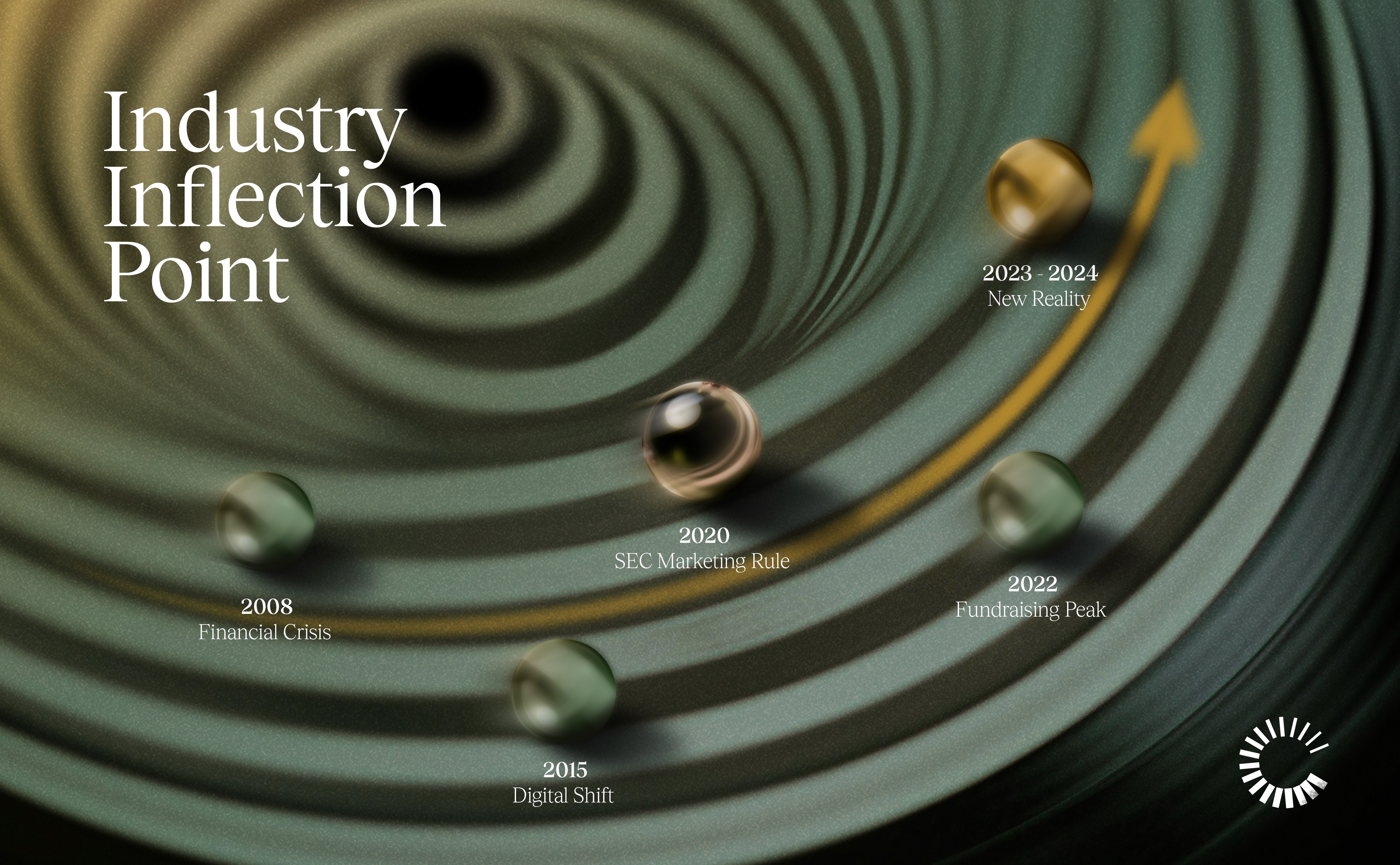

Five structural forces converged between 2008 and 2024 to fundamentally alter how capital gets raised.

1. The SEC's Marketing Rule

Adopted on December 22, 2020, the rule allowed investment advisers to communicate more broadly about performance and strategy with private fund investors. Well-intentioned transparency flooded the market with content. Allocators now face signal-versus-noise problems that didn't exist five years ago.

When every manager can share track record data and thought leadership, quality of communication becomes the filter.

2. Market saturation intensified competition for attention

After reaching peaks of more than 6,815 private equity funds worldwide and $1,152.74 billion raised in 2021, the market corrected sharply. The number of global private equity fund launches continued to decline.

Following 1,241 funds launched in the first half of 2024, the number dropped further to 479 in the first half of 2025. But capital availability contracted faster than fund supply. Allocators, facing diminished returns expectations and heightened risk awareness, concentrated commitments among fewer managers, leaving the remaining funds competing for a smaller allocation pool under tighter scrutiny.

3. Generational wealth transfer accelerated during this period

Cerulli Associates projects that wealth transferred through 2045 will total $84.4 trillion, accelerating the shift of decision-making authority to younger, digital-native allocators in family offices and endowments. These allocators research funds online before accepting meetings.

They evaluate websites, LinkedIn presence, and content quality as proxies for operational capability. Their discovery behavior differs fundamentally from the relationship-first approach of previous generations.

4. Operational due diligence deepened after 2008

LPs now evaluate culture, ESG integration, risk management frameworks, and how managers articulate strategy. ILPA's Due Diligence Questionnaire, (DDQ) updated throughout 2021 and again in 2023, standardizes these inquiries. Allocators compare DDQ responses against pitch decks and websites for consistency. Misalignment signals operational gaps.

5. Technology accessibility leveled the playing field

Tools that once required Fortune 500 budgets (sleek web platforms, professional design software, data visualization) became available to emerging managers. This democratization raised baseline expectations. No fund is "too small" for professional materials.

Why this makes communication a fundraising variable

These forces explain why fundraising, branding, and investor communications can no longer be separated. In saturated markets where dozens of funds post comparable returns, every external touchpoint must reinforce the same narrative. The investment thesis informs brand positioning. Brand positioning shapes fundraising conversations. Content strategy supports both.

This integration requires lead time. Positioning work ideally begins 12-18 months before fundraising launches. As one IR head quoted in Bladonmore's Raising the Bar report put it: "By the time it comes round to fundraising, you should have already built a relationship with that prospect in the same way that you do with an existing investor."

Managers who start communication planning when fundraising opens face compressed timelines that show in output quality.

How allocators make decisions now

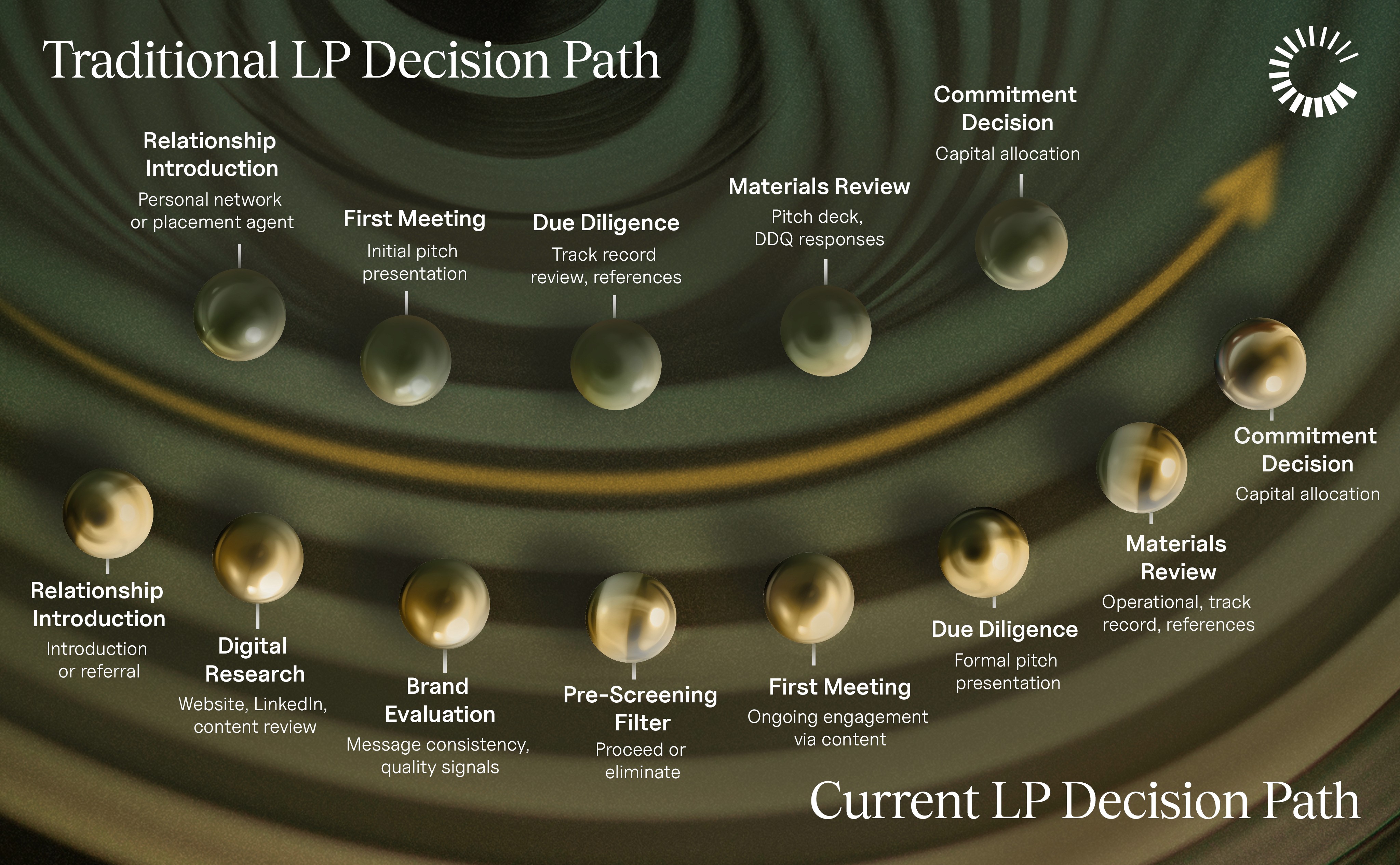

They use digital pre-screening.

The traditional path was linear: relationship leads to meeting, meeting leads to due diligence, due diligence leads to commitment. That model assumed allocators evaluated managers who reached their desk. Now, substantial filtering happens before first contact.

Industry practitioners like Matt Curtolo (private market expert from Allocate) emphasize the growing importance of digital brand presence, with fund managers facing heightened pressure to distinguish themselves through strategic digital engagement in a competitive landscape.

Before responding to manager outreach, allocators review websites, read thought leadership, assess LinkedIn profiles, and evaluate pitch materials for consistency and clarity. Digital presence functions as a pre-screening mechanism that determines which managers advance to conversation.

They check for brand coherence as a capability indicator.

When allocators encounter warning signs like inconsistent messaging between pitch deck and website, outdated content with no recent market perspectives, or DDQ responses written in a different voice than other materials, they often move managers from “active evaluation” to “monitor” status. None of these factors alone disqualifies a manager, but collectively, they could extend timelines by months.

The contrast with managers who maintain institutional-grade digital presence is striking. Clear strategy articulation, consistent messaging across platforms, regular market insights, and coordinated materials that answer allocator questions proactively can compress decision timelines and speed up fundraising cycles.

When these elements align, allocators move to first meetings sooner because the pre-screening phase has already built confidence.

What winning firms do differently

Firms closing funds efficiently treat every touchpoint as part of an integrated strategy.

Consistent narrative architecture across all materials

Pitch decks, DDQ responses, websites, thought leadership, and investor updates reinforce the same strategic narrative. The investment thesis articulated in a pitch deck matches the framing on the website. Risk management philosophy in DDQ responses aligns with quarterly letters. This consistency signals that the firm thinks systematically about positioning and communication.

Proactive visibility between fundraising cycles

Leading managers don't wait until fundraising to build their brand. They publish quarterly market perspectives, participate in industry forums, and maintain an active digital presence during investment periods.

This content serves dual purposes: it demonstrates analytical capability while keeping the firm top-of-mind when allocators have capital to deploy. Producing data-rich, high-quality research helps PE firms build trust and differentiate themselves, ultimately strengthening conversations with LPs.

The compounding effect matters. Managers who publish consistently build a body of work allocators can reference. When fundraising opens, they don't start from zero. Allocators have already formed impressions based on 12 or 18 months of content. The first meeting feels like a continuation, not an introduction.

Contrast this with managers who go silent between fundraises. When they resurface, allocators must rebuild context. The manager's positioning isn't clear, their market perspective isn't known and every conversation starts cold.

The timeline math is unforgiving. If fundraising can take 18 months and deployment can take 3-4 years, managers have roughly 24-36 months between active raises. Using that period to build visibility transforms the next fundraise. Ignoring it means repeating the same cold-start process with every cycle.

Allocator-centric messaging answers questions before they're asked

Instead of listing fund achievements, materials address LP concerns directly:

How does the risk management framework limit downside?

What operational principles ensure portfolio company value creation?

How does the team's experience translate to current market conditions?

This shift from manager-focused to allocator-focused communication accelerates decision-making.

The implications for fund managers

Communication investment is no longer optional.

It directly affects fundraising velocity and capital efficiency.

Timing matters.

Brand-building can't start when fundraising launches. Establishing credibility and recall with allocators requires 12-18 months of consistent presence. Managers who begin this work during investment periods approach fundraising with advantages: allocators will already know the firm, materials have been refined through multiple iterations, and messaging has been tested in real conversations.

Quality thresholds have risen across the market.

Allocators expect institutional-grade materials even from first-time funds. The bar moved from "good enough for our stage" to "indistinguishable from established firms." When technology makes professional output accessible to all managers, poor execution signals choice rather than constraint.

Emerging managers often underinvest, underestimating how much brand signals matter to allocators.

They assume performance will speak for itself, then extend fundraising timelines when materials quality slows decision-making. Top-quartile managers extend timelines when material quality or messaging clarity creates friction in allocator decision processes.

Competitive reality creates measurable advantages for firms that execute integration.

Close rates improve. Fundraising timelines compress. Allocator conversations start warmer and progress faster. The gap between leaders and laggards widens as more managers recognize the shift.

Relationships still create opportunities and brand quality helps convert them. Managers who execute both will close faster, so budget decisions should weigh communication infrastructure against its impact on fundraising outcomes, not against arbitrary cost targets.

How to build an integrated communication infrastructur

If you are preparing for your next raise or you are currently in the market, these practical steps can accelerate your progress:

1. Audit current materials for consistency.

Review your pitch deck, website, DDQ responses, investor letters, and any public content. Document where terminology, framing, or value proposition differs. Map gaps between how the firm describes itself across channels. This diagnostic reveals misalignment that allocators notice.

2. Define core positioning before creating materials.

Answer three questions clearly:

What makes this fund different from others in the segment?

What specific concerns do target allocators have, and how does the strategy address them?

What proof points demonstrate capability beyond track record?

Use these answers as architecture for all external communication.

3. Establish content rhythm 12-18 months before fundraising.

Publish quarterly market perspectives or annual outlooks that demonstrate analytical capability. Focus on allocator-relevant insights rather than marketing content. Build credibility and recall before capital raising begins.

4. Coordinate materials development strategically.

Your company website, pitch deck, and DDQ responses should be developed together or in sequence, not as separate projects. Ensure investment thesis, risk framework, and operational philosophy are described consistently. Test materials with friendly allocators and incorporate feedback before broad distribution.

5. Invest in relationships between cycles.

Use content and selective outreach to maintain connection with target allocators during investment periods. The goal is recognition and recall so that when fundraising opens, allocators already understand the firm's positioning and capabilities.

The bottom line

Brand and fundraising are now nearly synonymous. Every allocator touchpoint (how you communicate, present decisions, and articulate your strategy) shapes attention, trust, and commitment. The tools to compete are accessible, the playbook is clear, and the gap between leaders and laggards is still narrow enough to close if you move now.