Key takeaways

Co-investment reshapes GP revenue: The median fund loses 25% of effective fee income.

Fee compression hits record lows: Management fees fell to 1.61%, and won't recover.

LP leverage keeps tightening terms: Over half of LPs report stronger negotiating positions.

Platform scale determines survival options: Smaller firms face the squeeze without diversified revenue.

What's actually changing in GP economics

GPs raising capital right now face a question their fundraising materials rarely address: can the firm's economics survive the terms LPs are demanding? Co-investment rights that reduce effective revenue by 25% per fund. Management fees at their lowest recorded level. Transparency requirements that let allocators benchmark GP economics with unprecedented precision.

The largest platforms have responded by diversifying revenue well beyond fund management fees. Most firms below that threshold are absorbing the pressure with a narrower set of strategic options, and allocators are increasingly modelling GP economic sustainability as part of their diligence process.

The math behind 2/20 has quietly broken

Average buyout management fees fell to 1.61% in 2025, a record low and roughly 20% below the legacy 2% standard. But fee compression is the smaller problem.

The median GP now offers 33 cents of co-investment for every dollar of fee-bearing capital, reducing effective revenue per fund by 25% before a single portfolio company is acquired. Some managers offer as much as $1.10 per fee-bearing dollar, deploying roughly twice the capital they earn fees on.

For a GP running a $1B fund, this means:

Significantly less revenue to cover team, infrastructure, and reporting

More co-investors requiring governance and communication

More complex LP reporting and LPAC oversight

Operational costs expanding while the fee base contracts

Why this hits some firms harder than others

Two factors kept this from being a uniform story.

First, fee compression is concentrated in larger funds where economies of scale offset the rate decline. A $15B fund at 1.5% still generates $225M in management fees over the investment period. At those fund sizes, the math suggests that revenue per partner has grown even as fee rates declined.

Second, managers with strong DPI track records retain meaningful pricing power. More than half of LPs feel they hold more cards than a year ago, but that finding applies unevenly. First-time funds and managers carrying weak recent vintages absorb the brunt. A GP returning cash consistently still commands attention and premium terms.

Bain's characterization of a K-shaped recovery captures this dynamic: capital is flowing to a narrow subset of managers with strong track records and scale, while firms without either face a materially harder fundraising environment and greater pressure on terms.

Co-investment has become a revenue transfer, not a relationship tool

For most of the industry's history, co-investment was a way to deepen ties with anchor LPs and enable larger transactions. That framing no longer reflects how allocators think about it.

The numbers tell the story:

88% of LPs plan to allocate up to 20% of their portfolios to co-investments over the next five years

62% of LPs report being below target on co-investment allocations

CalSTRS removed its independent fiduciary verification requirement for co-investments under $250M, prioritizing speed in deploying fee-free capital

The calculus that makes co-investment attractive to LPs works in reverse for GPs.

The GP counterargument deserves weight

Co-investment enables deal sizes the fund couldn't reach alone, maintains LP relationships across fundraising cycles, and generates carry-on transactions that might not otherwise close. A manager pursuing a $2B acquisition with a $1B fund needs co-investment capital to compete. In that context, the "lost" management fee is offset by carrying on a deal the fund couldn't execute independently.

The 25% revenue reduction from Bain is a median across all respondents. Managers with proprietary deal flow and disciplined co-investment allocation face less dilution. But the question hanging over that selectivity is how long it remains viable as LP expectations converge toward universal access.

The "no fee, no carry" headline masks a more complex picture

Co-investments are marketed as fee-free, but portfolio company-level charges complicate that framing. Transaction fees typically run 1-3% of purchase price. Monitoring fees range from 1-3.5% of EBITDA or $1-10M annually. Because co-investment vehicles lack the management fee offset that fund LPs receive, co-investors bear these costs directly. Experienced allocators are increasingly focused on this interaction.

Pre-signing co-underwriting has grown fivefold over two decades, with co-investors assuming broken-deal costs and diligence burdens alongside GPs. Performance data shows 2.7x gross TVPI for pre-signing deals versus 2.2x for post-signing, which partly explains why LPs with the resources to participate early are pushing for earlier access.

How firm size determines what comes next

The largest platforms have built revenue models where traditional buyout economics represent one component among several.

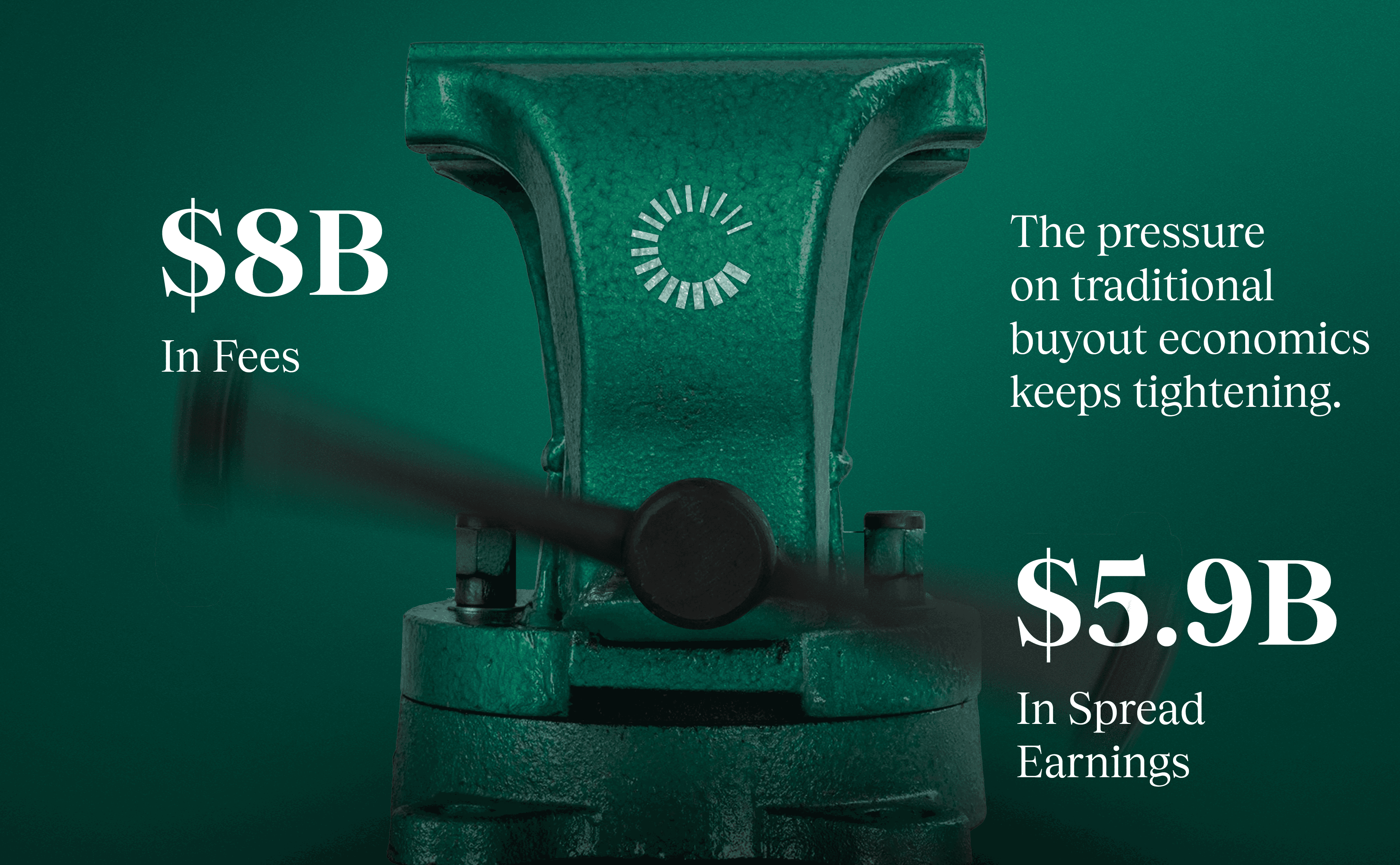

Blackstone generated $8 billion in net management and advisory fees in 2025, nearly three times its $2.8 billion in realized performance revenues. Apollo's combined fee and spread-related earnings reached $5.9 billion, with retirement services and credit origination contributing more than traditional fund management.

Their diversification playbook includes:

Private credit, where the top 50 firms raised 91% of capital in 2024 and concentration continued tightening in H1 2025, with 46% of all capital flowing to just 15 managers

Insurance balance sheets, providing permanent capital without fundraising cycles

Retail wealth products, with higher-liquidity vehicles growing 20-25% year-on-year in 2025

Defined contribution access, where 90% of GPs are interested and 24% are already designing products

Bain estimates that sovereign wealth funds and individual investors will contribute 60% of future AUM growth by 2033. Firms with infrastructure to access these channels are building revenue models that don't depend on traditional fund economics.

Managers below the mega-fund threshold face a narrower path

For firms that can't build credit platforms, launch retail products, or acquire insurance companies, the economic squeeze operates without a release valve. Smaller GPs face longer fundraising periods, making them more receptive to LP demands. The operational burden of co-investment programs falls on teams with less infrastructure to absorb it.

The viable path is narrower, though managers with demonstrable sector advantages have maintained pricing power. Sector specialization, proprietary deal flow, and repeatable operational value creation in markets the larger platforms can't or won't pursue remain genuine differentiators.

What has changed is that these advantages need to be articulated with precision in fundraising materials. The fee premium they justify is no longer assumed by allocators running comparative economics across their GP roster.

What happens when every line item is visible

ILPA's updated Reporting Template, effective 2026, standardizes how GPs disclose expenses, fees, and economics to LPs. The mechanical details matter less than the result: allocator teams can now run side-by-side comparisons of GP economics across their entire portfolio. Fee rates, co-investment ratios, and expense allocations become data points in a benchmarking exercise rather than outcomes of private negotiations.

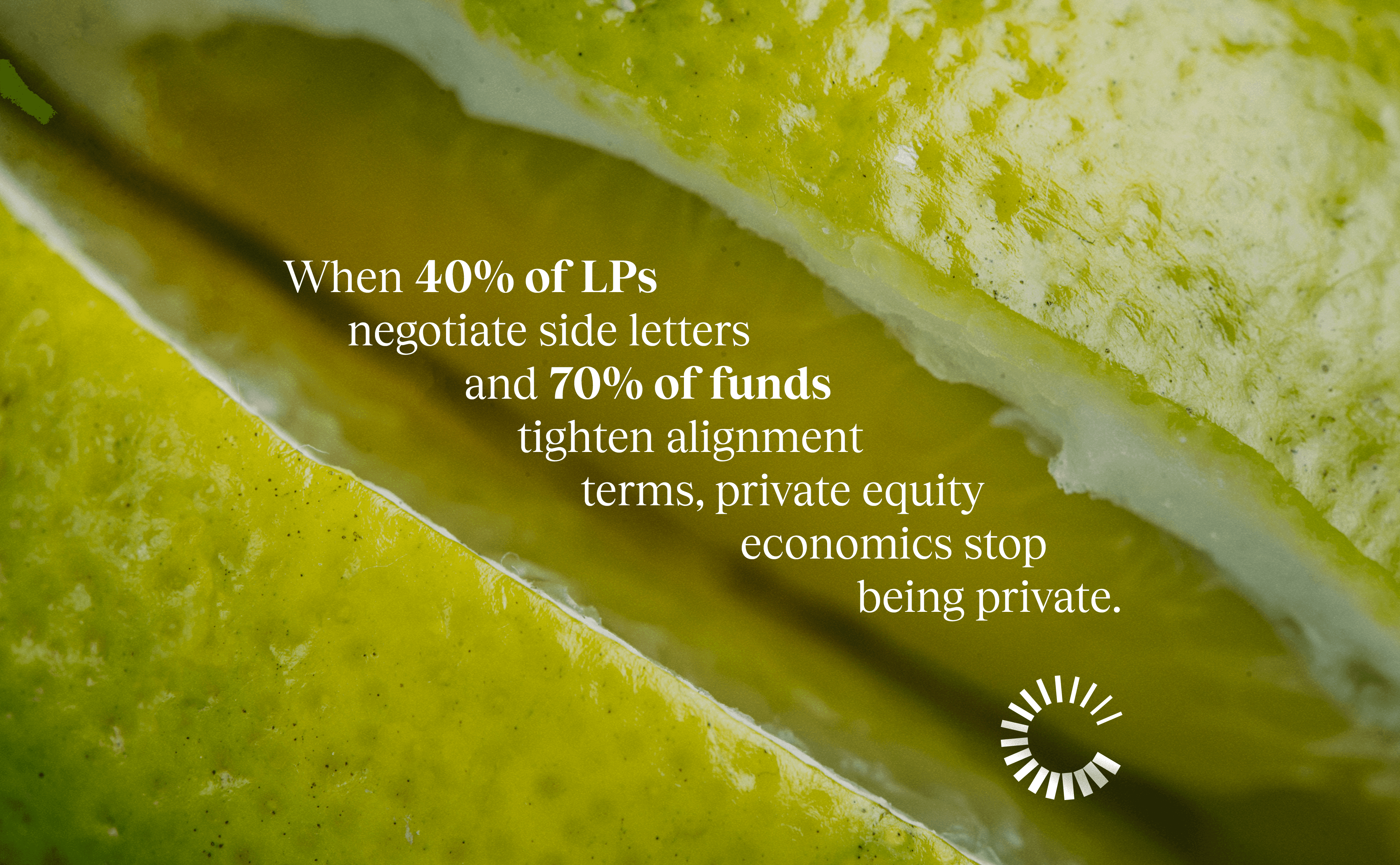

That transparency reinforces the co-investment pressure. When 40% of LPs are negotiating side letters and 70% of recent funds include tighter alignment terms (key-man clauses, enhanced clawbacks, expanded governance rights), fund economics are converging toward a visible market standard.

For fund managers, this changes what investor materials need to do. Presentations that describe co-investment as a "relationship benefit" without addressing its revenue impact risk reading as uninformed or evasive to an allocator who has already benchmarked the economics.

The firms navigating this well are direct about it: they explain how their fee structure supports the team, infrastructure, and reporting commitments that LPs are underwriting, at rates the market can verify.

Bottom line

The firms best positioned in this environment have aligned their economics with how they communicate. Fee structures, co-investment policies, and operational infrastructure tell a coherent story, while fundraising materials present it directly.

What's shifting is the selection criteria itself. Allocators aren't only comparing returns across managers. They're evaluating whether a GP's business model can sustain the team, systems, and institutional credibility that generated those returns, at the economics the market now requires.

For managers preparing their next raise, one question deserves attention before any material reaches an LP's desk: if an allocator models the firm's economics at current market fee rates (with the co-investment access they'll expect), does the picture hold together? Fee rates won't recover, but how a firm presents its terms can still shape how allocators perceive its durability.

Collateral Partners works with fund managers to build investor materials that address the questions allocators are already asking.