Key takeaways

Lending grew alongside trading. Banks are financing both companies and the buy side.

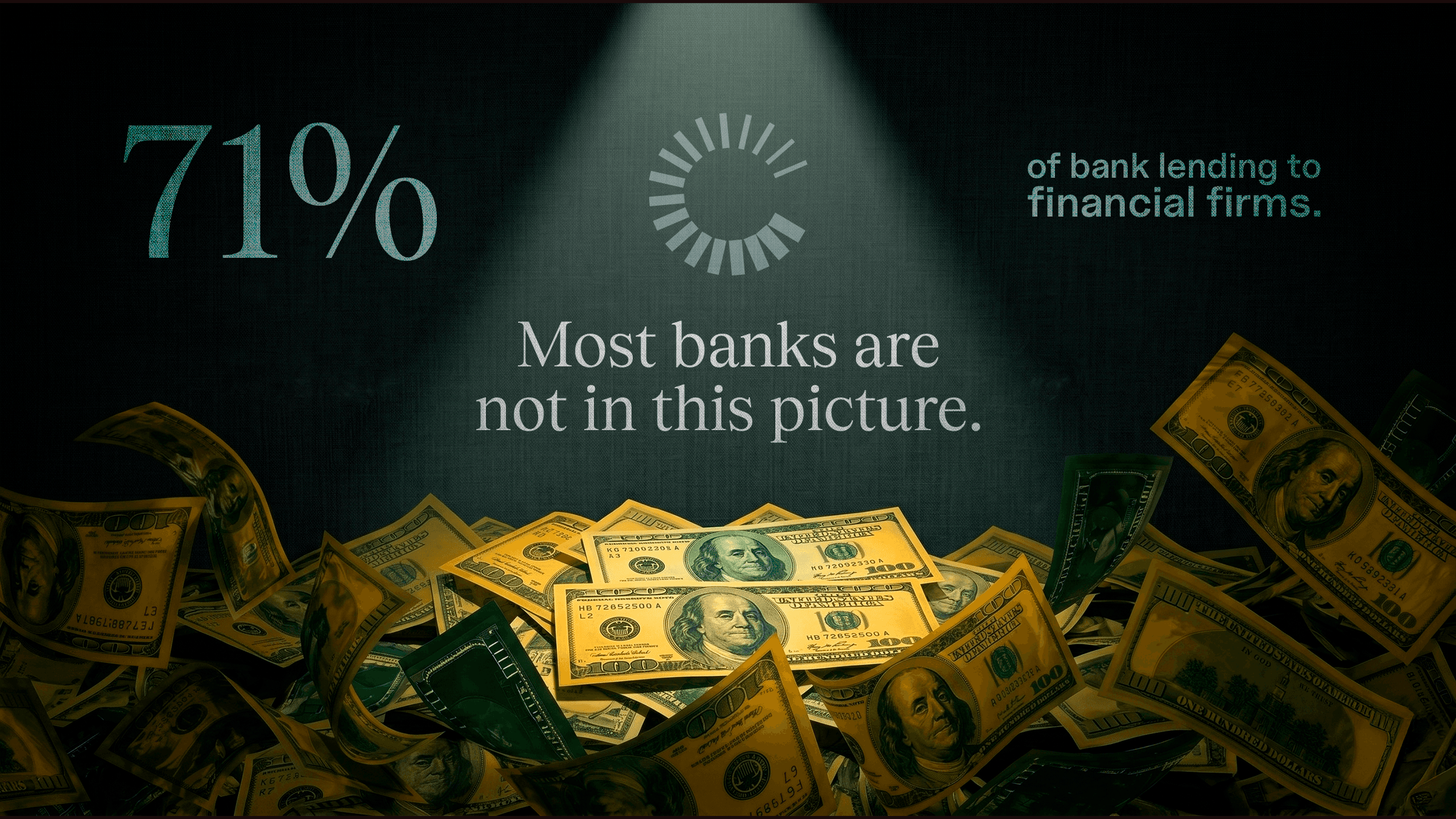

Ten banks dominate the system. 71% of lending to financial firms sits with these institutions.

The 2025 rule change is a tailwind. A regulatory shift made bank balance-sheet bets even more profitable.

Bank earnings are now LP signals. Counterparty concentration is rising as a fund diligence question.

The headline numbers hide a more useful story

The largest US banks just reported one of the strongest first quarters they have ever had. JPMorgan's markets revenue hit a record $11.6 billion. Goldman Sachs posted record equities revenue of $5.3 billion. Bank of America had its best equities trading quarter ever, up 30% year over year.

Most of the financial press read this as a Wall Street comeback driven by market volatility and a busier deal-making cycle. That story is true, but it misses the part that matters for anyone running a private-markets firm.

Both businesses grew. The more useful question is which grew fastest, and which clients moved to the front of the line. The answer reveals a pattern 15 years in the making — one that shapes how funds borrow from banks, how hedge funds access prime brokerage, and how LPs will read counterparty risk through 2026.

Loan books are growing but the borrowers are not who you’d think

Banks are not pulling back from lending. JPMorgan's loans grew 11% year over year. Bank of America's grew 9% to $1.19 trillion. Goldman's total loans rose from $210 billion to $253 billion, up 20%. So the easy story that banks are shifting from loans to trading does not hold up. The more interesting question is who the banks are lending to. And the answer reframes how to read the rest of the quarter.

The fastest-growing loans are going to other lenders, not companies

In February 2026, the FDIC published a report on bank lending to nondepository financial institutions, or NDFIs. They are the non-bank players that lend, invest, or finance things — private credit funds, hedge funds, asset managers, mortgage lenders, broker-dealers, REITs, and the financing facilities that fund private equity deals. They are the machinery of modern finance that sits next to banks rather than inside them.

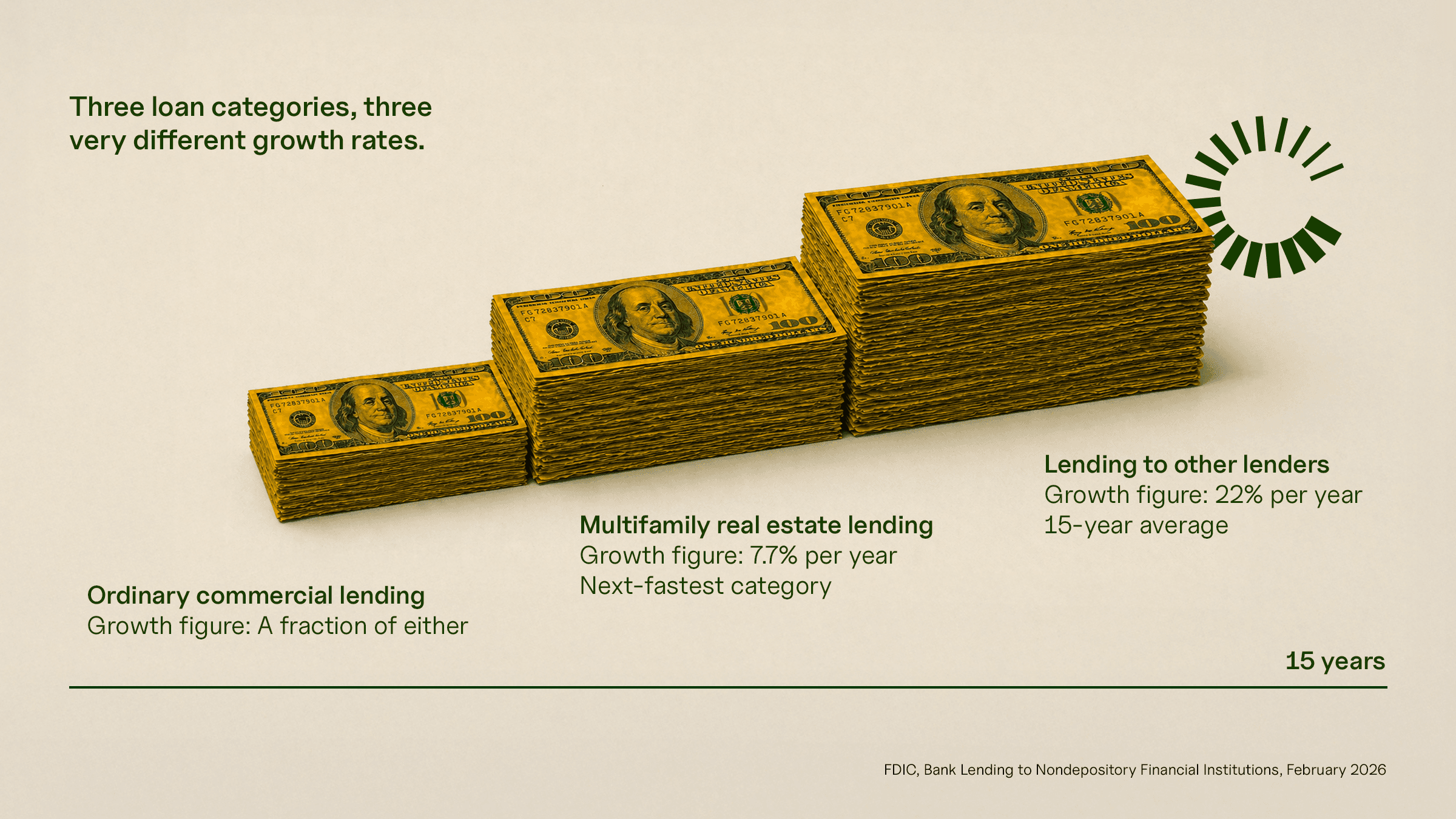

Lending to these institutions has been the fastest-growing loan category since the 2008 financial crisis. Three figures tell this story:

It has grown roughly 22% per year for 15 years, almost three times faster than the next-fastest loan category.

Outstanding loans to NDFIs reached $1.32 trillion by late 2025, equal to 10% of all bank lending.

Almost all of this lending sits at the largest banks — 10 institutions hold about 71% of it.

So banks have been growing their direct loans to companies, yes. But their loans to the institutions that lend to companies have been growing significantly faster for over a decade, and the activity is concentrated at the same handful of banks that just posted record trading numbers.

This isn't new. A handful of large banks have been quietly turning into the financial system's lender-to-lenders for over a decade. Q1 2026 just brought it into focus.

The trading desks are betting on the same clients

Reading the lending data alone, you might conclude that banks are more willing to lend to financial institutions than they used to be. That would be a credit story. The trading numbers tell you it's bigger than that. The fastest-growing parts of bank trading desks aren't just serving the same clients — they're built around lending to them.

Take Goldman's record equities quarter. Inside that result, the standout was prime brokerage — the business of lending money and securities to hedge funds so they can place larger trades. That business grew 59% annually. The rest of equities, where Goldman earns its money on trading rather than on financing, grew 7%.

Bank of America makes the point even more directly. Its Global Markets division, which houses its trading desks, grew its balance sheet by 14% to $1.1 trillion. Loans inside that division grew 26% — three times the bank's overall loan growth. The bank deliberately moved more of its money into the trading division so the trading desks could lend more to clients.

This is the part of the story the headline trading numbers obscure. The largest US banks are using every part of their balance sheet — loan books, trading desks, prime brokerage — to finance the buy side.

Is this just one unusual quarter? Bank of America has now posted 15 consecutive quarters of growing trading revenue. That's nearly four years of sustained build-up, not a one-time spike from a volatile few months. Banks have been deliberately and patiently reorganizing their capital around these clients.

A 2025 rule change just made this strategy more profitable

The structural pattern in lending and trading was already in place before regulators acted. But in November 2025, the Federal Reserve, OCC, and FDIC finalized a rule that rewards exactly this kind of business model. The rule took effect April 1, 2026.

What the rule actually does

The technical name for the rule is the enhanced supplementary leverage ratio — a regulation that tells banks how much capital they need to hold against the size of their balance sheet, regardless of how risky the underlying loans or trades are. Until now, this regulation was the binding constraint on the largest US banks, defining how much capital they had to hold.

The problem with that approach is that it treated all balance sheets equally:

Banks held the same amount of capital against a Treasury bond as against a junk loan.

That made low-risk activities like prime brokerage and lending to financial institutions surprisingly expensive in capital terms.

It nudged banks toward higher-risk activities to earn enough return on the capital they were forced to hold.

The new rule loosens that. The Fed itself says the change reduces capital requirements by "less than two percent" and that overall capital levels will be "broadly unchanged" — so headlines calling this a major capital giveaway are overstating it. It does, however, change the math on which businesses are profitable to grow.

Once leverage stops being the binding constraint, banks are once again rewarded for choosing low-risk activities, and the ones that benefit most are the same ones the Q1 2026 numbers showcased: prime brokerage, lending against capital commitments to private equity funds, and market-making in Treasuries.

A second rule change worth flagging

On December 5, 2025, the FDIC and OCC also rescinded a 2013 guidance document that had previously discouraged banks from making aggressive leveraged loans. That guidance was one of the reasons leveraged lending migrated to private credit funds in the first place. Removing it makes it easier for banks to do that lending themselves or, more likely, to keep financing the private credit funds doing it.

What the skeptics will say, and why the argument still holds

Three counterarguments are worth taking seriously before going further.

"Loan growth is strong everywhere, so the pattern isn't real"

Yes, total lending is up. But the growth is wildly uneven across categories, and the uneven distribution is the whole story.

Lending to other lenders has grown roughly 22% per year for 15 years

The next-fastest loan category, multifamily real estate, grew 7.7% per year over the same period

Ordinary commercial lending grew at a fraction of either rate

The skeptic is right that overall lending is healthy. The article does not claim otherwise. The claim is that the distribution of growth is so lopsided that calling it "general loan growth" misses where the action actually is.

"The NDFI growth numbers are inflated by an accounting change"

This is the sharpest objection. In late 2024, regulators changed how banks report their loans, and a chunk of what banks already had on their books got moved into the "lending to financial institutions" category. So roughly $334 billion in loans appeared to shift overnight without any new lending taking place (FDIC report - $193 billion in commercial loans and $141 billion in consumer loans). Some of the recent growth is just relabeling.

But the relabeling only affects the last year of data. The trend goes back fifteen years:

Lending to financial institutions has been the fastest-growing loan category since 2010

Strip out the relabeling effect entirely, and the growth rate moves from 22% per year to 21%

The same handful of large banks have been driving that growth across two different presidential administrations and three different sets of banking rules

The pattern was visible long before the accounting change.

"Trading was strong because markets were volatile, not because banks pivoted"

Markets were choppy, clients needed help managing positions, and trading desks were busy. Goldman's bond trading was actually down 10% in the same quarter — exactly the kind of inconsistency you'd expect if the story were just about volatility.

But the volatility argument can't explain the parts of the trading data that look sustained:

The fastest-growing trading business at Goldman was prime brokerage — lending to hedge funds — which grew nine times faster than the rest of the equities desk.

Bank of America moved 14% more of its overall capital into its trading division, a deliberate allocation decision rather than a reaction to one quarter.

BoA has now posted growing trading revenue for fifteen quarters in a row, a pattern stretching back nearly four years before any of the recent volatility.

A volatile quarter explains a spike. It does not explain a buildup that's been going on for years.

What this means for IR teams, fund CFOs, and allocators

IR and capital formation

LPs are about to start asking sharper questions about which banks finance the fund. The reason is visible in the data: 10 institutions hold about 71% of all bank lending to financial firms (FDIC report). That means most private credit and private equity managers depend on a smaller circle of banks than they probably realize, and almost always a smaller circle than their own LP base.

The implication is concrete:

LPs in 2026 will increasingly want to know which banks provide your fund's financing, on what terms, and what happens to the fund if one of them pulls back.

The risk is most acute around the $987 billion in financing commitments banks have promised but not yet drawn, which could land on the same banks at the same time during a market stress (FDIC report).

IR teams that can walk an LP through this calmly will handle the conversation well; those treating it as a back-office detail will not.

This connects to a broader pattern in how LP diligence evolves across the fund lifecycle, where the operational and counterparty questions LPs ask now arrive earlier in the process than they used to.

Fund CFOs and finance leads

The cost of borrowing from banks is about to change shape, even if the headline rates don't move much. Until now, the rules forced banks to treat all loans roughly the same way for capital purposes, which made low-risk lending less profitable than it should have been.

The 2025 rule change means that banks will now be rewarded for choosing low-risk borrowers, and they'll price their loans accordingly:

Larger funds with strong track records and existing relationships will get better pricing and more flexible terms.

Smaller or newer funds, or those with less established bank relationships, will likely face the opposite.

Refinancing in 2026 is a moment to rethink which banks the fund is using, not just to assume current pricing will continue.

Allocators evaluating credit managers

A private credit manager whose financing comes from one or two of the 10 banks that dominate this kind of lending carries a very different risk profile from one with financing spread across several. If one of those banks pulls back, the manager's ability to operate normally pulls back with it.

Bank lending decisions in 2026 will shape which managers can grow and at what cost. The implication for allocators:

A manager's bank lineup is now part of the risk evaluation, not just a back-office question.

Managers who depend on a small number of banks are more exposed to bank policy shifts than their loan books suggest.

Concentration in bank relationships rarely shows up in pitchbook materials but increasingly belongs in diligence questions.

This connects to broader questions about how fund market positioning shapes capital allocation, where the bank-relationship layer is one of the harder-to-see things LPs evaluate but rarely ask about directly.

These are interpretations, not predictions. They could shift if interest rates move sharply, or if the next round of bank rule-making lands very differently from what's currently expected.

Bottom line

The interesting question for the rest of 2026 is what will happen to these patterns when the next stress event arrives. NDFI lending currently shows a 0.15% past-due rate, well below the 1.32% rate on traditional C&I loans.

That looks like prudent underwriting, and at the loan level, it largely is. But the FDIC's own report flags two pressure points: $987 billion in unfunded NDFI commitments that could land on bank balance sheets simultaneously in a stress, and a generation of NDFI counterparties that has not been tested through a full credit cycle.

For practitioners, the analytical work splits accordingly. GPs should be modeling what happens when the bank on the other side of their facility is fielding draw requests from 10 other GPs at the same time. Allocators should be looking past loan-level metrics and into network-level concentration, which has not been tested.

Read this way, public-bank disclosures become a map of who finances whom rather than a quarterly scoreboard. That kind of structural framing increasingly shows up inhow funds with the strongest LP retention communicate during periods of market stress, and it's the kind of work Collateral Partners builds with managers preparing for that level of LP scrutiny.