Key takeaways

First impressions determine whether LPs evaluate your performance. Pattern recognition from reviewing hundreds of managers creates unconscious filters that operate in under 2 minutes, often screening managers out before their track record receives serious consideration.

Credibility signals are proxies for operational competence. Visual consistency, data formatting, assumption transparency, and structural logic all communicate analytical rigor and back-office discipline. LPs interpret these details as indicators of how managers will perform over a seven-year fund life.

Transparency builds trust more than aggressive projections. Conservative framing with explicit sensitivity analysis gains more credibility than optimistic base cases without downside exposure. Approximately 69% of institutional investors now spend more time on due diligence as they become more selective.

Consistency across touchpoints matters as much as individual materials. Discrepancies between websites, pitch decks, and communications trigger concerns about strategic clarity and institutional coordination that extend beyond marketing into operational questions about team alignment.

Limited partners make critical credibility judgments in the minutes before a pitch call begins. Pattern recognition from reviewing hundreds of fund managers creates unconscious filters that operate before rational performance analysis starts, determining whether LPs engage deeply or screen out early.

What LPs evaluate in the first 90 seconds

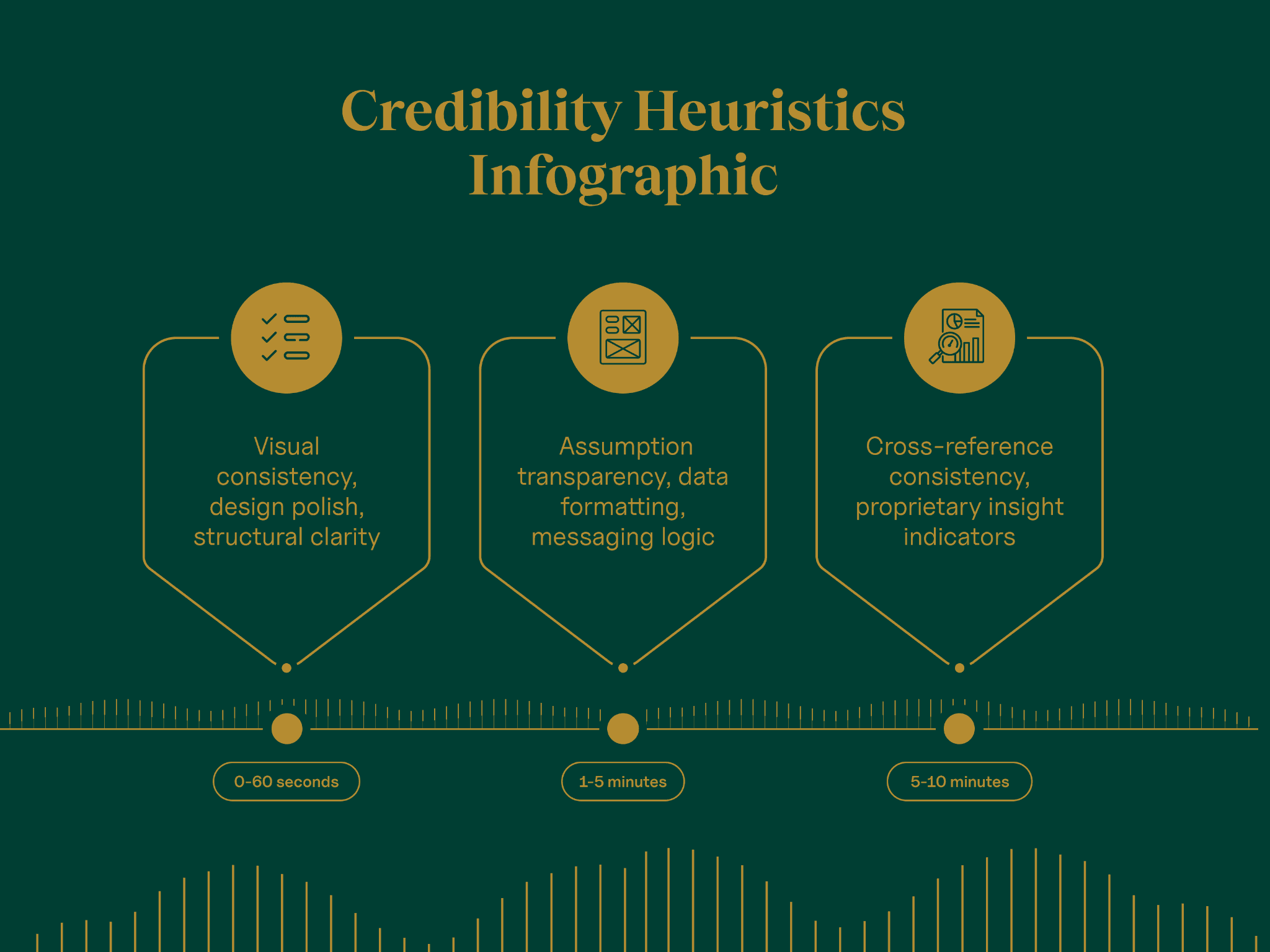

Allocators develop screening heuristics after years of evaluating managers. Institutional investors form preliminary assessments in less than 2 minutes of reviewing materials. These initial judgments rarely reverse, even when subsequent performance data looks strong.

Visual consistency signals operational discipline. Misaligned tables, inconsistent fonts across slides, or poorly formatted numbers trigger pattern recognition developed from seeing hundreds of decks. LPs interpret these details as proxies for back-office competence. If a manager can't maintain consistent formatting across 15 slides, the investor will question their ability to maintain consistent reporting across a seven-year fund life.

Data formatting reveals analytical rigor before anyone discusses returns. Numbers rounded to logical increments (2.4 billion, not 2,378,456,892), sources clearly cited, and assumptions explicitly stated all communicate methodological discipline. Materials that bury exit cap assumptions in footnotes or use vague qualifiers like "substantial market opportunity" fail the transparency test most allocators apply unconsciously.

Structural logic matters more than managers realize. Does the deck open with market context before strategy, or jump straight to portfolio companies? Do sections flow in the sequence LPs use for mental due diligence? Allocators evaluate thousands of investment opportunities using established cognitive frameworks. Materials that match those frameworks feel immediately coherent.

Industry guidance and pitch-deck best practice recommend leading with market opportunity and narrative flow because first impressions strongly affect whether allocators proceed to deeper diligence.

How assumption transparency builds LP trust

Allocators screen for whether managers state assumptions explicitly or leave them for LPs to discover. This distinction separates managers who understand institutional expectations from those still operating with high-net-worth investor norms.

Conservative framing builds credibility even when projections are optimistic. LPs expect sponsors to provide sensitivity analysis and stress tests for key assumptions in their financial underwriting, with more sophisticated limited partners adjusting GP assumptions based on their own experience to develop conservative assessments.

Consider this scenario as an example: A real estate fund targeting 18% net IRR gains trust by showing sensitivity analysis at 15%, 18%, and 21% scenarios with clearly stated cap rate and rent growth assumptions. An identical fund loses credibility by presenting 18% as the base case without showing downside exposure or assumption dependencies.

Two funds with similar historical performance can generate opposite credibility assessments based on how they disclose modeling choices:

Fund A presents projected returns with a detailed assumptions page: acquisition cap rates, renovation costs per unit, stabilized occupancy targets, exit cap rate range, and hold period.

Fund B presents identical return projections with generic "conservative underwriting" language and no quantified parameters.

LPs engage Fund A for deeper diligence. Fund B triggers skepticism about what else might be obscured.

The transparency paradox creates tension managers must navigate. Detailed assumption disclosure builds trust but exposes strategy specifics that some managers prefer to share only after NDAs. Most allocators, however, won't sign NDAs before seeing enough detail to justify diligence time. ILPA’s templates and standards emphasise transparency and standardisation of manager disclosures in initial and ongoing investor materials. While many GPs prefer to withhold certain strategic assumption details prior to NDAs, the market expectation is increasingly for more upfront disclosure to build trust with allocators.

Regional differences matter here. European allocators generally expect more assumption detail upfront than US family offices, which may accept broader ranges initially. Pension funds typically require comprehensive sensitivity analysis before first meetings, while some high-net-worth offices engage first and request details later. These patterns are reflected in CFA Institute survey data on allocator practices, which highlight that European investors often have stricter governance and reporting expectations compared with counterparts in the Americas and other regions.

Design quality as operational proxy

Visual polish correlates with back-office competence in LP psychology, whether managers find that fair or not. The Cambridge Associates’ 2024 Manager Guide emphasizes the importance of operational infrastructure and personnel in manager evaluation, highlighting that managers need to be sufficiently resourced to trade and execute transactions efficiently.

The causation runs backward from what managers expect. LPs don't think "good design means good operations." Instead, they pattern-match: Managers with institutional operations consistently produce institutional-quality materials. Materials that don't meet that standard trigger questions about what else might be missing.

Polish doesn't require expensive agencies. Consistency matters more than production value. A deck using standard fonts throughout, with aligned tables and uniform spacing, signals more care than an over-designed presentation with inconsistent formatting. Modest but consistent quality across all materials have far greater impact than a beautiful deck and a sub-standard quarterly report.

The Fortune 500 peer test provides a useful benchmark. Would these materials fit in a board presentation alongside established institutional managers? Not "could they compete with Goldman Sachs marketing," but "do they look appropriate for serious capital allocation conversations?"

Some allocators prefer understated materials. A segment of European family offices and certain institutional investors view highly produced decks with suspicion, associating them with marketing over substance. These allocators prioritize data density and analytical depth over visual appeal. Managers raising from multiple allocator types must balance these preferences to present themselves professionally competent without being slick.

Visual breakdown of signal categories (design, data, structure, consistency)

Time-based: what LPs assess in first 60 seconds vs. first 10 minutes

Consistency across touchpoints

Limited partners notice discrepancies between websites, pitch decks, one-pagers, and email communications. These inconsistencies trigger concerns about institutional coordination that extend beyond marketing into operational questions.

If, for example, a hedge fund used a deck that described a "market-neutral equity strategy" during a fundraising process while their website emphasized "alpha generation through directional positioning", it would create a messaging gap. Even though both descriptions may be technically accurate for different fund components, a CIO might question whether the investment team had clear strategic consensus.

Materials should reflect a single institutional narrative. Investment thesis, competitive positioning, risk framework, and performance attribution should use consistent terminology across every investor touchpoint. When a deck references "value-add repositioning" but the website describes "opportunistic real estate," LPs wonder whether the firm has defined its market position.

Email signatures, proposal letters, and follow-up materials all contribute to pattern recognition. A fund that maintains professional consistency in major presentations but sends follow-up emails with inconsistent formatting or casual language undermines the institutional impression it worked to create.

This doesn't mean rigidity. Firms evolve, strategies adapt, and messaging should reflect genuine changes. The issue arises when simultaneous materials tell different stories, suggesting either unclear strategy or inadequate coordination between team members responsible for investor communication.

The relationship between credibility signals and due diligence depth

Strong first impressions change how allocators evaluate subsequent performance data. LPs who form positive initial assessments spend more time in detailed diligence and interpret ambiguous information more charitably. Weak first impressions trigger confirmation bias toward screening out, where LPs scrutinize for reasons to decline rather than reasons to advance.

A 2023 survey by Private Equity International revealed that 69% of institutional investors reported spending more time on fund due diligence as they become more selective. This indicates a significant increase in the time allocators dedicate to evaluating potential investments. The depth of engagement differs substantially based on presentation quality and structural clarity.

This isn't about deceiving allocators. Managers with strong track records deserve fair evaluation of their performance. First-impression risk prevents that fair evaluation from occurring. An emerging manager with top-quartile returns may never get serious consideration if materials signal "not yet institutional-ready" in the first five minutes.

The mechanism operates through time allocation. LPs review far more opportunities than they can fund. Initial screens determine which managers receive thorough performance analysis, reference calls, and operational due diligence. Managers screened out early rarely realize they never reached the stage where their track record would have differentiated them.

Investment consultants describe this as the "presumption of competence" threshold. Materials that meet institutional standards create a presumption that the manager belongs in serious consideration, shifting the burden toward finding reasons to move forward. Materials that fall short create a presumption of early-stage development, shifting the burden toward finding exceptional reasons to override concerns.

Family offices vs. endowments vs. pension funds

Which signals matter most to each segment

Regional and segment variations

US family offices often accept broader initial materials with less assumption detail, preferring to request specifics during follow-up conversations. European institutional investors typically expect comprehensive disclosure upfront, including detailed sensitivity analysis and explicit risk frameworks.

These differences stem from due diligence culture and regulatory context. European allocators operate under stricter disclosure regimes and have developed expectations accordingly. US investors, particularly in private wealth segments, often rely more heavily on relationship trust and accept staged information disclosure.

Pension funds and endowments typically prioritise assumption transparency and data rigour over design flourishes. Investment committees and trustees expect documentation that supports fiduciary decision-making, which means managers should present explicit, quantified assumptions and clear sensitivity or scenario analysis rather than only high-level visuals or marketing copy. Institutional best-practice guides and standardised LP due-diligence templates make clear that reasoned assumptions, documented rationale and reproducible analysis are core to materials that can be defended to a board.

Family offices span the widest range. Some operate with institutional rigor matching pension funds. Others take an entrepreneurial approach, making decisions on relationship and conviction with less formal documentation. Materials designed for one family office segment may feel over-engineered or under-documented for another.

Emerging managers receive some accommodation, but less than many assume. Allocators distinguish between "early-stage but institutional trajectory" and "not yet ready for institutional capital." A first-time fund without comprehensive infrastructure gets understanding about operational limitations. That same fund loses credibility if materials suggest it doesn't understand what institutional standards require.

Established funds face different expectations. A manager on Fund IV should demonstrate institutional polish that a debut fund might still be building. LPs interpret presentation quality from established managers as revealing true operational maturity, not just marketing budget.

Common credibility killers managers don't see

Overloaded slides signal unclear thinking rather than thoroughness.

Allocators interpret dense pages as evidence that managers can't distinguish critical information from supporting detail. A slide containing 12 bullet points, three charts, and two data tables suggests the manager either doesn't know what matters most or can't prioritize effectively.

Vague quantifiers undermine analytical credibility.

Phrases like "substantial deal flow," "significant market opportunity," or "strong investor demand" without supporting data make allocators question whether actual metrics would support the claims. If you are concerned about disclosing competitive information, you should use ranges ("50-75 opportunities reviewed quarterly") rather than unquantified assertions.

Mismatched terminology between sections reveals coordination gaps.

When executive summary language differs from detailed strategy description, or when financial projections use different return metrics than performance track record sections, LPs notice. These inconsistencies suggest either careless assembly or unclear communication between team members.

Generic market analysis fails to demonstrate proprietary insight.

Allocators see the same macro trends cited across hundreds of decks. Materials that reference standard industry reports without connecting to specific investment implications waste credibility-building opportunities. Managers differentiate by showing how they interpret widely available information differently, not by summarizing what everyone already knows.

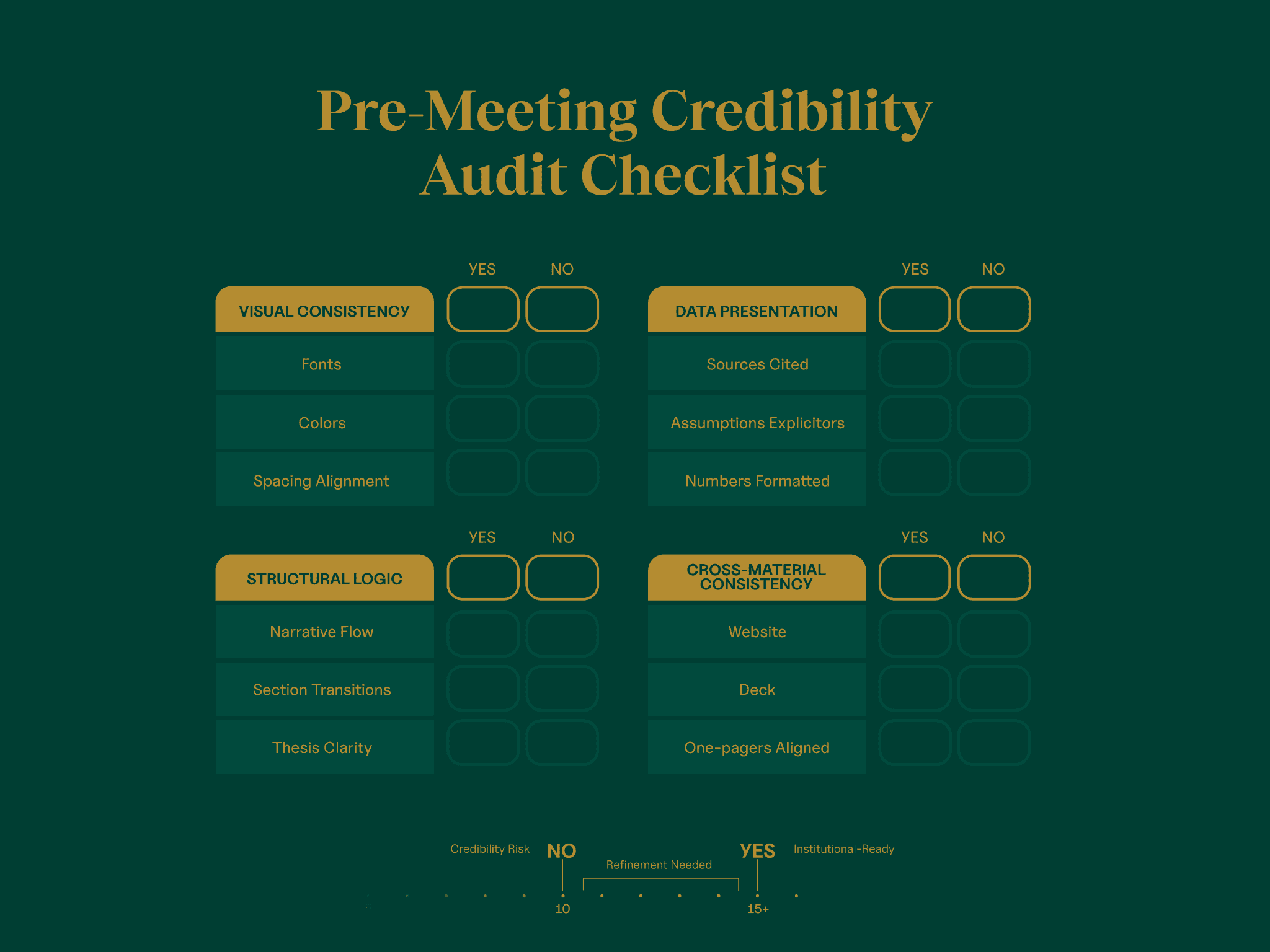

Credibility audit checklist:

Every data point includes source and timeframe

Assumptions stated explicitly, not buried in footnotes

Consistent terminology across all sections

Visual formatting uniform throughout

Each slide communicates one clear idea

Supporting detail available but not cluttering main narrative

Market analysis connects directly to investment strategy

Risk discussion balances opportunity presentation

How to audit materials against institutional standards

1. The peer comparison test for positioning

The peer comparison test reveals positioning gaps. Would your materials fit naturally in a stack alongside top-quartile managers in your segment? Not "are they as expensive to produce," but "do they communicate at the same level of institutional sophistication?" Internal teams become blind to their own materials after multiple revisions, making honest external perspective essential for accurate assessment.

2. The allocator speed-read test for structural clarity

The allocator speed-read test measures structural clarity. Can an informed peer understand your investment thesis, competitive advantage, and risk profile in under five minutes? Time yourself presenting only the information visible on slides without verbal elaboration. LPs often review decks before calls without managers present to explain, so materials must stand alone.

3. The consistency audit for alignment across touchpoints

The consistency audit examines all investor touchpoints systematically. Create a spreadsheet listing how you describe strategy, positioning, and competitive advantages across websites, pitch decks, one-pagers, email templates, and proposal letters. Terminology discrepancies that seem minor in isolation compound into credibility concerns when LPs cross-reference materials.

4. The decision point for visibility before execution

The decision point isn't "can we make these changes ourselves" but "do we see what needs changing?" Managers who recognize specific gaps can often execute corrections internally, particularly if team members include former allocators or institutional communications professionals. Those uncertain whether materials meet institutional standards benefit from external review by professionals who understand LP psychology and can identify blind spots internal teams miss.

Self-assessment tool managers can apply to their materials

Signal categories with yes/no evaluation criteria

Practical action steps

Use the LP Credibility Audit Checklist to assess where your materials sit on the institutional-readiness spectrum. Then conduct your consistency audit by documenting how you describe strategy, positioning, and competitive advantages across all investor touchpoints.

Ask an informed peer outside your organization to complete the five-minute allocator read test and summarize your core narrative. Request feedback from friendly allocators or investment consultants who can provide honest assessment of where materials fall on the emerging-to-institutional spectrum.

Schedule a consultation with Collateral Partners for professional assessment of credibility signals in your current materials and strategic guidance on closing institutional-readiness gaps efficiently.

The bottom line

Performance remains the foundation of any institutional relationship, but first-impression credibility determines whether LPs engage deeply enough to evaluate your track record fairly. Pattern recognition from reviewing hundreds of managers creates unconscious filters that operate before rational analysis begins, making these heuristics predictable enough to audit against.

Most credibility signals stem from consistency, transparency, and structural logic—elements you control regardless of fund size or marketing budget. Your materials either earn serious consideration or screen you out before performance data matters, making this one of the few fundraising variables you can fix before the next LP conversation.