Key takeaways

Volatility drives collateral, not price. Sustained swings raise margin demands even when prices stabilize.

Inflation expectations move first. Breakevens reprice within hours, ahead of official data.

Correlation compresses collateral buffers. Diversified collateral pools can behave as single exposures under stress.

Persistence is the key variable. Short-lived spikes fade; sustained volatility becomes a funding event.

Why this matters for balance sheets now

Most coverage of the Iran strikes has focused on oil prices, safe-haven flows, and the question of whether the Strait of Hormuz closes. For institutional balance sheets, the more immediate issue is less visible: how sustained energy volatility can move through inflation expectations, margin models, and collateral frameworks fast enough to create funding demands before risk teams have finished reading the headlines.

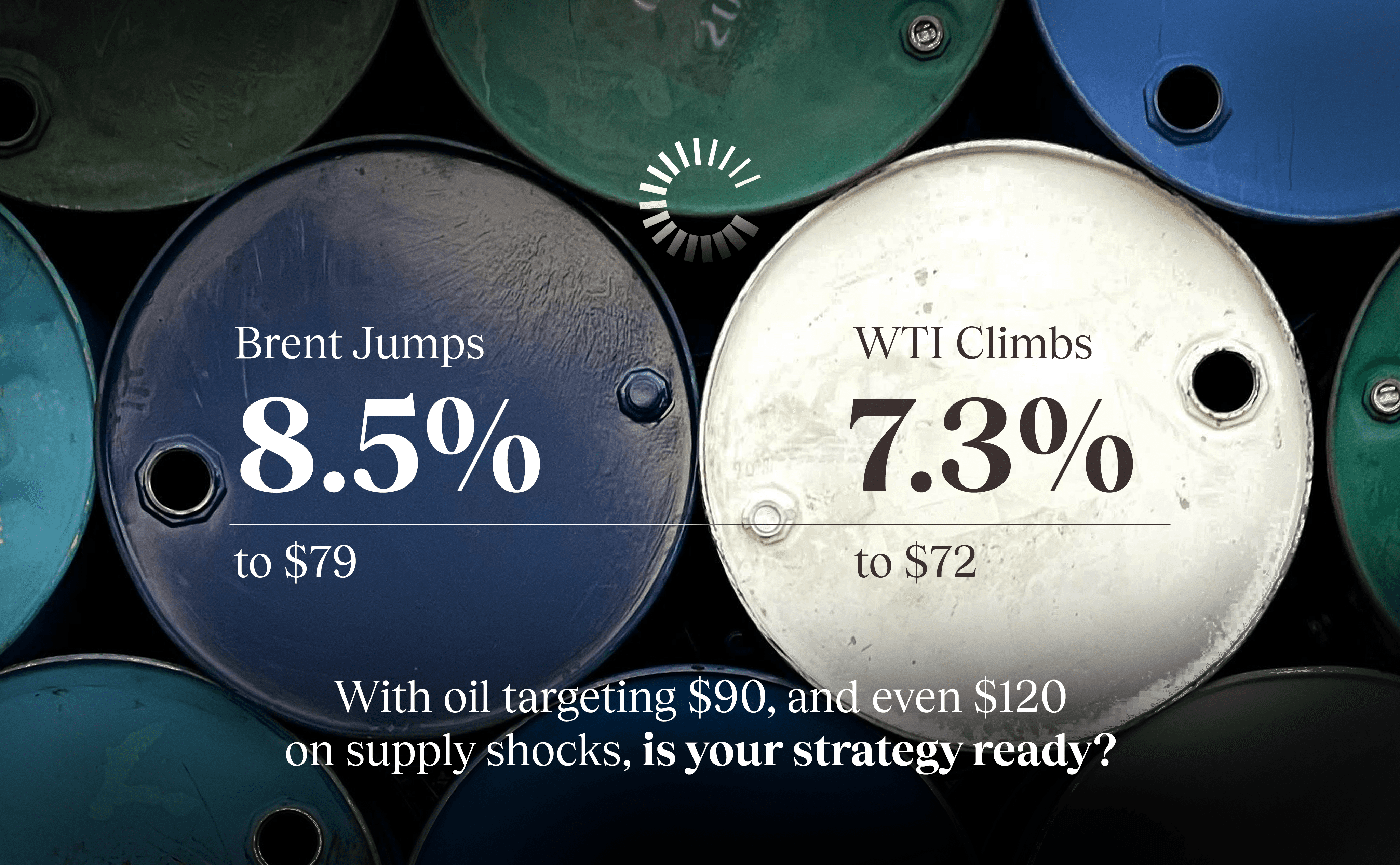

Brent crude surged more than 8.5% to around $79 per barrel on Monday following coordinated US and Israeli strikes on Iran, with West Texas Intermediate up roughly 7.3% to ~$72. Analysts at Barclays have warned that Brent could trade between $80 and $90 in the coming days, with UBS flagging the possibility of prices above $120 if supply through the Strait of Hormuz is materially disrupted.

That corridor carried an average of 20 million barrels per day in 2024, representing roughly one fifth of global petroleum liquids consumption, according to the US Energy Information Administration. For institutional investors and treasury teams, the question is how sustained price swings feed into funding and collateral mechanics.

Oil moves first, everything else follows

A sustained move above historical norms feeds directly into risk models that calibrate margin, credit exposure, and portfolio value-at-risk. The recalibration moves through several channels:

Energy-intensive corporates face earnings pressure that can widen credit spreads on their debt, forcing portfolio repricing across affected holdings.

Sovereign borrowers in oil-importing economies may see currency and bond market strain, particularly across Asia, where 84% of crude transiting Hormuz was destined in 2024.

Commodity-linked derivatives positions face rising collateral demands as clearinghouses recalibrate to reflect the new volatility regime.

Iran's retaliatory strikes against oil tankers near the Strait of Hormuz in the Middle East have already led to more than 200 vessels, including oil and liquefied gas tankers, halting in the strait and surrounding waters rather than transiting.

Saudi Arabia and the UAE maintain bypass pipeline capacity, but combined alternative routes cover roughly one third of aggregate Gulf export flows. The remaining two thirds have no physical alternative.

Funding desks don't need to predict where oil settles. They need to determine whether the current volatility regime has persisted long enough to trigger recalibration in their margin models, credit assessments, and collateral eligibility frameworks. For most cleared derivatives, that threshold is measured in days, not weeks.

Inflation expectations shift before central banks do

The 5-year breakeven inflation rate tracked by the Federal Reserve Bank of St. Louis tends to adjust within hours of a significant crude move, well ahead of official CPI releases.

That speed matters for two connected reasons:

Rising breakevens shift rate path expectations, which feeds directly into duration pricing across fixed income portfolios.

If expectations move high enough to challenge the rate-cut trajectory markets had been pricing, real yields adjust. That recalibrates discount rates across equities and credit simultaneously.

When risk premia move without economic deterioration

The IMF's April 2025 Global Financial Stability Report documented how geopolitical risk events can raise sovereign risk premia and trigger equity declines, with the impact particularly pronounced in markets with limited fiscal buffers. Its October 2025 report noted that financial conditions can tighten through rising risk premia and stretched valuations even while underlying economic data remains stable.

For collateral-dependent portfolios, this dynamic creates a compounding problem. Asset prices can decline (reducing collateral value) while margin requirements rise (increasing collateral demand). Both forces operate through the same volatility channel.

Collateral demands rise faster than most teams expect

Margin models are built to cover potential losses under extreme scenarios, typically targeting 99% of anticipated price moves. They rely on recent and implied volatility as core inputs. When volatility rises, collateral requirements rise with it.

That relationship is by design, but the side effects are well documented. During the COVID market turmoil in March 2020, margin demands spiked sharply and unpredictably, straining liquidity across the system. When commodities markets convulsed again in 2022 following the Ukraine invasion, clearinghouses faced similar pressure and several revised their stress testing approaches in response.

Since then, reforms have followed. CME Clearing, for example, now uses volatility floors and built-in buffers to reduce the likelihood of sudden margin increases during stress periods. ESMA finalized revised anti-procyclicality standards for European clearinghouses in 2023. For the largest clearinghouses, the infrastructure is better prepared than it was in 2020. Whether that preparation is sufficient under a compound stress scenario involving energy, rates, and geopolitical risk simultaneously remains untested.

But better preparation does not mean the cycle is broken. For portfolios with derivatives exposure across equities, rates, and commodities, even a modest percentage rise in required margin can mean a significant jump in the cash that needs to be posted.

Variation margin creates timing risk

Variation margin is calculated and settled daily, with intraday calls possible during elevated market movement. The obligation is immediate. Asset repositioning or collateral substitution in thinner markets is not.

This timing mismatch is where liquidity strain materialises for otherwise solvent portfolios. The BIS documented this dynamic during COVID: large US commercial banks doubled their cash assets between late February and early April 2020, partly in anticipation of margin calls. That hoarding behaviour itself intensified the liquidity squeeze, creating a feedback loop between margin demands and funding availability.

The current environment carries a similar structural risk. If oil volatility persists and cross-asset correlations rise, variation margin obligations could accelerate at the same moment that secondary market liquidity for risk assets contracts.

The assets everyone wants are the same ones you need to post

Treasuries and the US dollar attract flows during geopolitical stress. Gold has followed the same pattern, with spot prices rising sharply as investors seek hedges outside the credit system. But unlike Treasuries, gold does not function as eligible collateral in most clearing frameworks, which limits its role in the margin and funding transmission chain this article addresses.

When demand for high-quality liquid assets concentrates, repo rates can tighten and the availability of eligible collateral narrows. The New York Fed tracks Treasury market liquidity indicators that can signal these conditions. Treasury market functioning has improved since the March 2020 dislocation, when the Fed ultimately intervened to restore liquidity.

But improvement in normal conditions does not guarantee resilience during a concentrated stress event that combines energy supply disruption, inflation repricing, and geopolitical escalation simultaneously. The question is what happens to collateral pools when the assets inside them stop behaving independently.

When everything drops together, diversification disappears

Correlation convergence during stress is familiar territory. The less familiar question is what it does to collateral buffers when multiple margin exposures are backed by assets tied to the same economic drivers.

The diversification benefit that existed on paper evaporates in practice, triggering haircut recalculations and additional posting requirements across several counterparty relationships at once.

The practical issue is concentration:

How many margin obligations rely on similar asset types?

If those assets weaken together, what is the incremental funding requirement?

Answering these questions converts correlation from a market statistic into a projected cash outflow, which is the metric that funding desks can actually act on.

What to review now

The actionable response is arithmetic, not directional:

Margin elasticity. Model how a sustained increase in implied volatility, say two to three standard deviations above the trailing 90-day average, across core exposures would affect initial margin requirements. Convert potential volatility shifts into projected capital needs in dollar terms.

Collateral concentration. Identify assets posted as collateral across multiple counterparty relationships. Assess whether energy-sensitive credits, inflation-linked instruments, or correlated equity positions account for a disproportionate share of eligible collateral.

Haircut sensitivity. Review counterparty agreements and clearing arrangements to determine how haircuts adjust under stress scenarios. Some agreements reference specific volatility thresholds. Confirm where those thresholds sit relative to current market conditions.

Liquidity timing. Certify access to same-day or next-day liquidity sufficient to meet variation margin calls under a scenario where multiple positions require simultaneous posting. Ensure committed credit facilities align with potential intraday demands.

Indicator monitoring. Track oil implied volatility alongside price levels. Monitor the5-year breakeven inflation rate, investment-grade and high-yield credit spreads, and clearinghouse communications regarding margin methodology adjustments. These indicators provide earlier signals than headline price moves.

Bottom line

Markets are not pricing systemic failure. They are pricing uncertainty about how long disruption might last, and duration is what turns market swings into funding pressure.

If energy markets settle quickly, margin and collateral effects are likely to remain manageable. If disruption persists, adjustments to margin requirements and collateral valuations can build over time, narrowing liquidity buffers.

The operational risk lies in timing. Margin calls are daily. Collateral is revalued on set schedules. Funding access requires coordination. When those timelines tighten at once, liquidity, not solvency, becomes the immediate issue.

For continued analysis on margin, liquidity, and collateral dynamics, visit the Collateral Partners blog.